NOT AN OFFER TO SELL OR SOLICITATION OF AN OFFER TO BUY SECURITIES

PLEASE CAREFULLY READ THE FOLLOWING TERMS BEFORE USING THIS WEBSITE (“Site”). All persons using the Site expressly agree to the foregoing disclaimer as a pre-condition to using this Site for any purpose whatsoever. Continued use of the Site signifies your acceptance of, and agreement to be bound by, each and every one of the following terms and conditions.

The information on this Site is for informational purposes only, and is not an offering of or a solicitation to purchase securities or otherwise make an investment. Securities may only be offered or sold pursuant to registration of securities or an exemption therefrom using offering documents and sales of securities will be limited strictly to those persons who are qualified as “accredited investors” as defined in Regulation D promulgated under the United States Securities Act of 1933. Material information is detailed in the offering documents, including, but not limited to, risk factors.

Everything communicated by MVRK, LLC, Maverick Properties & Investments, LLC and its affiliates and agents, regardless of whether it is written, spoken, recorded audio or video, is intended for education and informational purposes only. All comments are solely the opinion of the presenter. Regardless of whether spoken or written, nothing shall be considered as giving investment advice, an offer, or solicitation, to buy and/or sell any type of investments products or securities. Prior to making any investment you should consult with a professional financial advisor, legal and tax advisor to assist in due diligence as may be appropriate and determining the appropriateness of the risk associated with a particular investment.

All information contained herein is provided “as is,” and MVRK, LLC, Maverick Properties & Investments, LLC and its affiliates each expressly disclaim making any express or implied warranties with respect to the fitness of the information contained herein for any particular usage, its merchantability or its application or purpose. In no event shall MVRK, LLC, Maverick Properties & Investments, LLC or its affiliates be responsible or liable for the correctness of any such material or for any damage or lost opportunities resulting from use of this data.

No action has been or will be taken to permit an offering of securities in any state where action would be required for that purpose. In considering any prior performance information presented on this Site, bear in mind that past performance does not indicate future results, and that there can be no assurance that comparable results will be achieved by MVRK, LLC, Maverick Properties & Investments, LLC or its affiliates. Moreover, any such past performance information is subject to, and should be reviewed in light of the assumptions accompanying that information. The use of terms such as higher, above average, safe or successful, express the opinion of MVRK and are not a promise or guarantee for any possible investment performance or safety of principal.

The sketches, renderings, graphics materials, plans, specifications, terms, conditions and statements contained in this Site are proposed only, and MVRK reserves the right to modify, revise or withdraw any or all of the same in its sole discretion and without prior notice.

MVRK, LLC, Maverick Properties & Investments, LLC as well as the logos and marks included on the Site that identify services and products, are proprietary materials. The use of such terms and logos and marks without the express written consent of Maverick Properties & Investments, LLC is strictly prohibited. Copyright in the pages and in the screens of the Site, and in the information and material therein, is proprietary material owned by Maverick Properties & Investments unless otherwise indicated. The unauthorized use of any material on the Site may violate numerous statutes, regulations and laws, including, but not limited to, copyright, trademark, or trade secret laws.

Additional Information from the SEC regarding 506C and 506B offerings

Advertising Approved for Unregistered Securities Offerings

The SEC’s Office of Investor Education and Advocacy is issuing this Investor Alert to educate individual investors about advertisements and announcements for investment opportunities in certain securities offerings. General advertising is permitted in certain offerings as a result of rules adopted by the SEC as required by the Jumpstart Our Business Startups (JOBS) Act.

You may begin to see advertising and announcements for opportunities to invest in certain securities offerings, some-times called private placements. These offerings may be for shares in a company or interests in a private fund, such as a hedge fund or venture capital fund. The advertising may be through a number of different means, including the Internet, social media, seminars, print, or radio or television broadcast. The rules permitting this general advertising take effect on September 23, 2013.

What is a private placement?

A securities offering exempt from registration with the SEC is sometimes referred to as a private placement. Under the federal securities laws, a company or private fund may not offer or sell securities unless the offering has been

registered with the SEC or an exemption is available. Private and public companies engage in private placements to raise funds from investors. Private funds, such as hedge funds, also raise investment capital through private placements.

Private placements are not subject to some of the laws and regulations that are designed to protect investors, such as disclosure requirements that apply to registered offerings.

as noted above, the SEC recently adopted rules to permit general solicitation or advertising for certain securities offerings that are exempt from registration. as described below, these offerings, referred to here as Rule 506(c) offerings, must comply with a number of requirements.

Am I qualified to invest in a Rule 506(c) offering?

Only accredited investors may invest in a Rule 506(c) offering. This limitation exists because these offerings do not have the same investor protections as, and have unique risks when compared to, offerings that are registered with the SEC.

an accredited investor, in the context of an individual investor, is a person who:

- had income in excess of $200,000 (or $300,000 with a spouse) in each of the prior two years, and reasonably expects the same for the current year, OR

- has a net worth over $1 million, either alone or with a spouse (excluding the value of the person’s primary residence or any loans secured by the residence (up to the value of the residence)).

How will the company or private fund know whether I am an accredited investor?

In a rule 506(c) offering, the company or private fund is required to take reasonable steps to verify your accredited investor status, which could include reviewing documentation, such as W-2s, tax returns, bank and brokerage statements, credit reports and the like. Depending on the circumstances, the company or private fund may rely on a written confirmation from a third party to verify your accredited investor status. The SEC does not require any specific verification method or process for companies or private funds for these offerings.

Third-party verification. If the company or private fund accepts a written confirmation from a third party to verify whether you are an accredited investor, the third party may be a registered broker-dealer, SEC-registered investment adviser, licensed attorney or certified public accountant. The third party could be engaged by the company or private fund, or could be retained by you (e.g., your personal broker-dealer, investment adviser, attorney or certified public accountant). You can obtain information about a registered broker by visiting FInra’s BrokerCheck website. You can obtain information about an investment adviser by visiting the SEC’s Investment adviser Public Disclosure (IaPD) website. You can obtain information about a licensed attorney or certified public accountant by contacting the appropriate state bar or board of accountancy.

You do not have to provide any information if you do not feel comfortable doing so. If you do not provide all of the requested information, you should not be able to invest in the particular offering if the company or private fund is unable to verify that you are an accredited investor.

If the company or private fund offering the securities does not take steps to verify your accredited investor status or allows you to participate in the offering even though you do not meet the income or net worth criteria discussed above, this may be a warning sign that the company or private fund is not complying with the federal securities laws and is something to consider before investing in the offering.

Investor Bulletin: Accredited Investors

The SEC’s Office of Investor Education and Advocacy is issuing this Investor Bulletin to educate individual investors about what it means to be an “accredited investor.”

What does it mean to be an accredited investor?

Under the federal securities laws, a company or private fund may not offer or sell securities unless the transaction has been registered with the SEC or an exemption from registration is available. Certain securities offerings that are exempt from registration may only be offered to, or purchased by, persons who are accredited investors. One principal purpose of the accredited investor concept is to identify persons who can bear the economic risk of investing in these unregistered securities. Unlike offerings registered with the SEC in which certain information is required to be disclosed, companies and private funds, such as a hedge fund or venture capital fund, engaging in these exempt offerings do not have to make prescribed disclosures to accredited investors. These offerings, sometimes referred to as private placements, involve unique risks and you should be aware that you could lose your entire investment. The SEC recently adopted rules to permit general advertising for certain exempt offerings.

Are you an accredited investor?

An accredited investor, in the context of a natural person, includes anyone who:

- earned income that exceeded $200,000 (or $300,000 together with a spouse) in each of the prior two years, and reasonably expects the same for the current year, OR

- has a net worth over $1 million, either alone or together with a spouse(excluding the value of the person’s primary residence).

On the income test, the person must satisfy the thresholds for the three years consistently either alone or with a spouse, and cannot, for example,satisfy one year based on individual income and the next two years based on joint income with a spouse. The only exception is if a person is married within this period, in which case the person may satisfy the threshold on the basis of joint income for the years during which the person was married and on the basis of individual income for the other years. In addition, entities such as banks, partnerships, corporations, nonprofits and trusts may be accredited investors. Of the entities that would be considered accredited investors and depending on your circumstances, the following may be relevant to you:

- Any trust, with total assets in excess of $5 million, not formed to specifically purchase the subject securities, whose purchase is directed by a sophisticated person, or

- Any entity in which all of the equity owners are accredited investors.

In this context, a sophisticated person means the person must have, or the company or private fund offering the securities reasonably believes that this person has, sufficient knowledge and experience in financial and business matters to evaluate the merits and risks of the prospective investment.

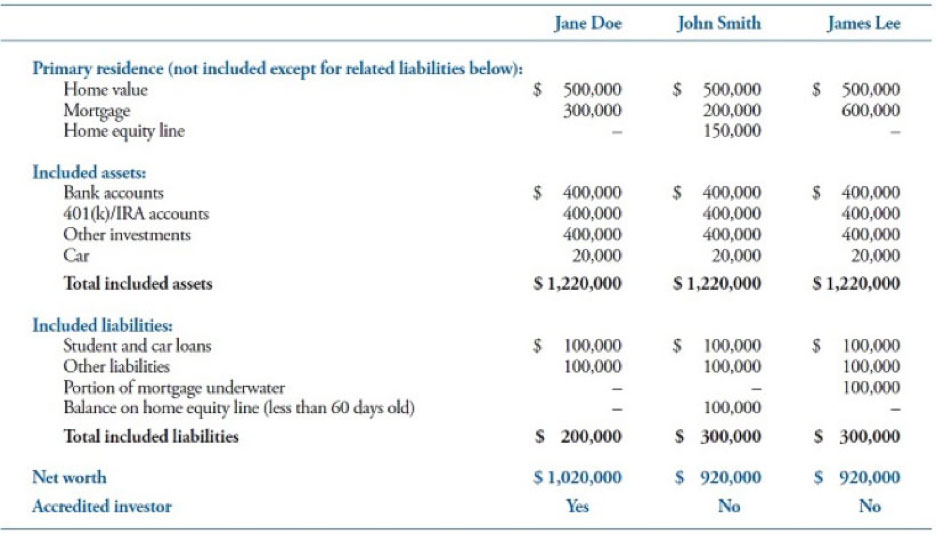

How do I calculate my net worth?

To qualify as an accredited investor under the net worth test, you must have a net worth that exceeds $1 million, either alone or with a spouse. If calculating joint net worth with a spouse, it is not necessary that property be held jointly. Calculating net worth involves adding up all your assets and subtracting all your liabilities. The resulting sum is your net worth.

The value of your primary residence is not included in your net worth calculation. In addition, any mortgage or other loan on the residence does not count as a liability up to the fair market value of the residence. If the loan is for more than the fair market value of the residence (i.e., if your mortgage is underwater), then the loan amount that is over the fair market value counts as a liability under the net worth test. Further, any increase in the loan amount in the 60 days prior to your purchase of the securities (even if the loan amount does not exceed the value of the residence) will count as a liability as well. The reason for this is to prevent net worth from being artificially inflated through converting home equity into cash or other assets.

The following table sets forth examples of calculations under the net worth test for being an accredited investor:

The rules defining accredited investor were changed with the passage of the Dodd-Frank Act to exclude a primary residence from the net worth test. This means that some investors who were accredited investors prior to July 20, 2010 are now not accredited investors. For these investors, any purchase rights, such as preemptive rights or rights of first offer, related to securities that they invested in as accredited investors prior to July 20,2010 are grandfathered in, provided that certain conditions are met. This means that the investor can still exercise these rights even though the investor may not meet the current definition of accredited investor.

Additional Information

For our Investor Bulletin about hedge funds, visit sec.gov/investor/alerts/ib_hedgefunds.pdf.

For our Investor Alert about general advertising for private placements, visit sec.gov/investor/alerts/ia_solicitation.pdf.

For FINRA’s BrokerCheck resource, visit www.finra.org/Investors/ToolsCalculators/BrokerCheck/.

For our Investment Adviser Public Disclosure (IAPD) website, visit www.adviserinfo.sec.gov.

For more information about certain exemptions for private placements, visit sec.gov/answers/regd.htm.

For our “Rule 144: Selling Restricted and Control Securities,” visit sec.gov/investor/pubs/rule144.htm.

For additional investor educational information, see the SEC’s website for individual investors, investor.gov.

The Office of Investor Education and Advocacy has provided this information as a service to investors. It is neither a legal interpretation nor a statement of SEC policy. If you have questions concerning the meaning or application of a particular law or rule, please consult with an attorney who specializes in securities law.

SEC Guidelines on Proving Accredited Status

What are Reasonable Steps?

So, what are reasonable steps to verify accredited investor status? The answer is: It depends. The SEC has adopted a “principles-based method” of accredited investor verification, indicating that the reasonable steps that are necessary to give an issuer a “reasonable belief” that all investors are accredited depends on the following factors:

- the nature of the purchaser and the type of accredited investor,

- the amount and type of information that the issuer has about the purchaser, and

- the nature of the offering, such as the manner in which the purchaser was solicited.

The SEC gives certain examples in the final SEC Regulations implementing Rule506(c), discussing how the reasonable steps necessary to verify accredited investor status depend on the facts and circumstances. For Example, “An issuer that solicits new investors through a website accessible to the general public, through a widely disseminated email or social media solicitation, or through print media, such as a newspaper, will likely be obligated to take greater measures to verify accredited investor status than an issuer that solicits new investors from a database of pre-screened accredited investors created and maintained by a reasonably reliable third party.” Another example is as follows: “…if the terms of the offering require a high minimum investment amount and a purchaser is able to meet those terms,then the likelihood of that purchaser satisfying the definition of accredited investor may be sufficiently high such that, absent any facts that indicate that the purchaser is not an accredited investor, it may be reasonable for the issuer to take fewer steps to verify or, in certain cases, no additional steps to verify accredited investor status other than to confirm that the purchaser’s cash investment is not being financed by a third party.”

Safe Harbor for Reasonable Steps

Fortunately, in the final release adopting Rule 506(c), the SEC adopted a non-exclusive “safe harbor” to provide some certainty that issuers are complying with the reasonable steps requirement for natural person investors. Provided that the issuer of securities does not otherwise have knowledge that such person is not an accredited investor, the issuer will be deemed to have taken reasonable steps if:

- with respect to purchasers who are accredited investors based on income, the issuer reviews IRS forms that report revenue (W-2, Form 1099, Schedule

- K-1 or filed Form 1040) for the last two years and obtains a written representation from such person that he or she has a reasonable expectation of reaching the income level in the current year;

- with respect to purchasers who are accredited investors based on net worth, the issuer reviews bank statements, brokerage statements, other statements of securities holdings, certificates of deposit and/or tax assessments and appraisal reports issued by third parties in order to verify assets, a consumer report from at least one of the nationwide consumer reporting agencies to verify liabilities and obtains a written representation that all liabilities necessary to make a net worth determination have been disclosed (all information reviewed may not be more than 3 months old);

- the issuer has obtained a written confirmation from a broker-dealer, a registered investment advisor, a licensed attorney or a CPA that such person has taken reasonable steps to verify that the purchaser is an accredited investor within the prior 3 months and determined that such purchaser is an accredited investor, and

- for purchasers who previously purchased securities in an issuer’s Rule 506(b)transaction prior to the effectiveness of Rule 506(c), a certification that such person is an accredited investor.

Although the safe harbors outlined above are not mandatory and are non-exclusive, most issuers with individual purchasers will likely take all necessary means to fall within the safe harbors because nobody wants to be one of the SEC’s initial test cases regarding whether the issuer of securities has taken reasonable steps.

Private placements – Rule 506(b)

Section 4(a)(2) of the Securities Act exempts from registration transactions by an issuer not involving any public offering.

To learn more about Section 4(a)(2), please click the box below.

Section 4(a)(2)

Rule 506(b) of Regulation D is considered a “safe harbor” under Section 4(a)(2). It provides objective standards that a company can rely on to meet the requirements of the Section 4(a)(2) exemption. Companies conducting an offering under Rule 506(b) can raise an unlimited amount of money and can sell securities to an unlimited number of accredited investors. An offering under Rule 506(b), however, is subject to the following requirements:

- no general solicitation or advertising to market the securities

- securities may not be sold to more than 35 non-accredited investors (all non-accredited investors, either alone or with a purchaser representative, must meet the legal standard of having sufficient knowledge and experience in financial and business matters to be capable of evaluating the merits and risks of the prospective investment)

If non-accredited investors are participating in the offering, the company conducting the offering:

- must give any non-accredited investors disclosure documents that generally contain the same type of information as provided in registered offerings (the company is not required to provide specified disclosure documents to accredited investors, but, if it does provide information to accredited investors, it must also make this information available to the non-accredited investors as well)

- must give any non-accredited investors financial statement information specified in Rule 506 and

- should be available to answer questions from prospective purchasers who are non-accredited investors

Purchasers in a Rule 506(b) offering receive “restricted securities.” A company is required to file a notice with the Commission on Form D within 15 days after the first sale of securities in the offering. Although the Securities Act provides a federal preemption from state registration and qualification under Rule 506(b), the states still have authority to require notice filings and collect state fees.

Rule 506(b) offerings are subject to “bad actor” disqualification provisions.

Relevant FAQs